FDR Had Macro Tools, We Need Micro Tools

With the development of Gross Domestic Product, New Deal state planners had the macroeconomic tools they needed to take on the Great Depression. To better direct its firehose of public investment, the modern state needs new microeconomic tools and its own mechanics to work with them.

Practically everyone has heard of Gross Domestic Product (GDP). For some, it is the yardstick for economic progress. For others, GDP is everything wrong with how economic policy is constituted—a number that reduces the myriad of welfare effects and experiences to a thing called “growth.”

GDP is both simpler and far more complicated than any of these things. At its core, GDP is an accounting convention for tracing sources and uses. It’s a way of organizing data into something that is relatively legible and comparable. Like any accounting identity, it has its corresponding balancing items. While GDP is an expenditure approach to accounting for economic activity, gross domestic income (GDI) is an incomes approach to the same activity. Knowing these relationships can tell you quite a bit about the social relationships underpinning economic activity.

But this piece is not about GDP. It is about why GDP emerged, and what it can teach us about the gaps in our knowledge. GDP is the product of the Great Depression and the Keynesian revolution. When the New Deal began, there was literally no way for economists, activists, or leaders to describe the effects of the crisis they were undergoing. Stories of Roosevelt administration officials counting railway cars as a proxy for economic activity abounded. In fact, we did not even understand the concept of the “macro-economy” as a measurable object until Keynes began to create a theory for it.

The Depression era, like the post-2009 “Great Recession,” was a macro-economic crisis. As a macro-economic variable, GDP could tell us a lot about the failure of macro-policy. This was a “Keynesian moment.”

In 2023, however, we are in a very different place. Labor markets are tight and unemployment low. The U.S. government is spending $1.7 trillion on new investments into green technology. All of this creates micro-level distortions in an economy firing on all cylinders. In this situation, unlike a century before, it is not enough to solve macro-coordination problems. We must also solve micro-coordination problems to make sure we are producing what we need and when we need it, so that we do not have price distortions as the result of bottlenecks.

We need, in other words, to bring back a concept we have not used in a while: planning within the context of a market economy. Not Soviet-style command planning but monitoring by a “bottleneck detective.”

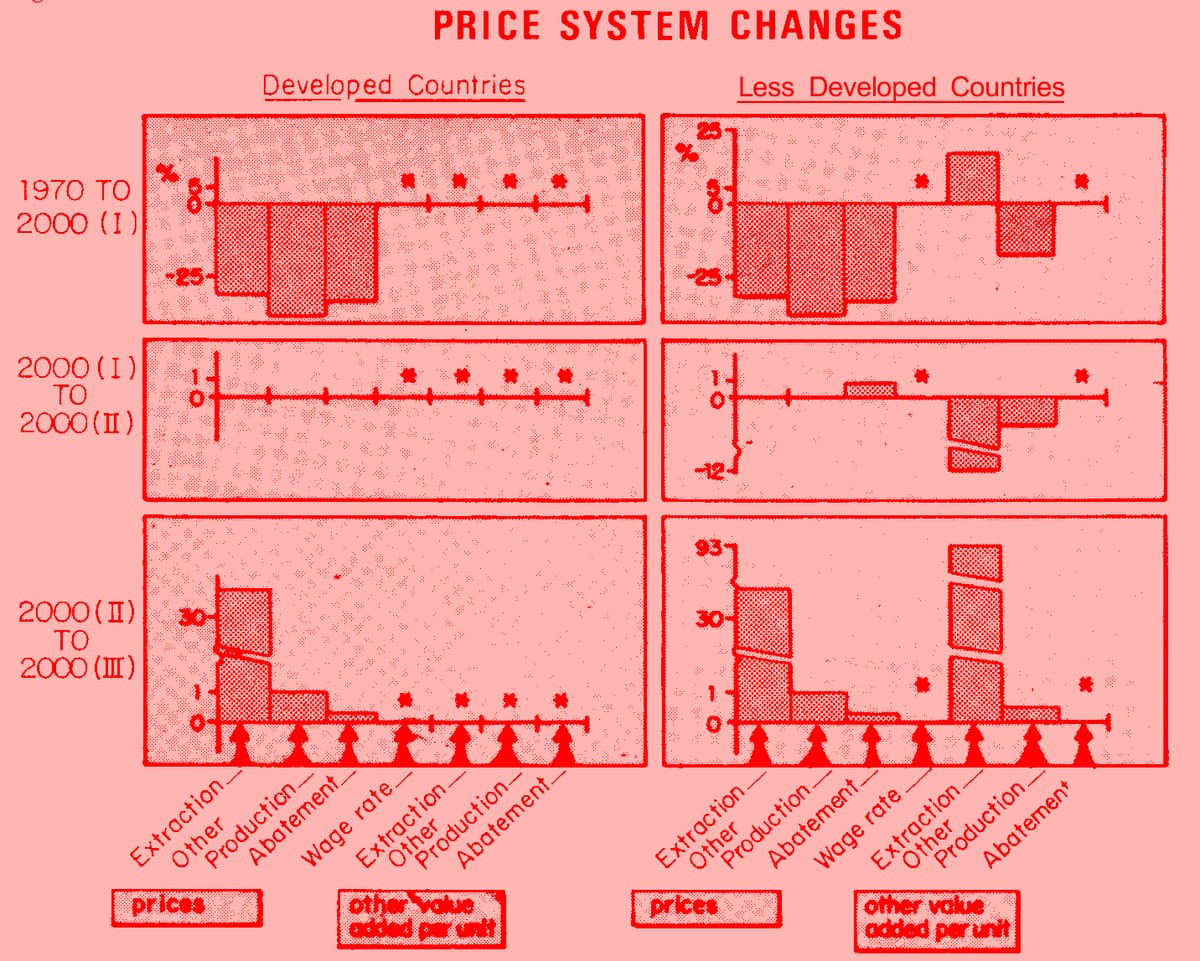

For the state to play such a role, we need a different set of numbers that goes deeper than GDP—microdata, along with the capacity to work with it. Wassily Leontief and his “input-output” economics (I-O) offers a lead here. I-O is a tool to understand how the addition of value flows through specific economic activity between sectors, like the interaction of components involved in mining, manufacturing, and the generation of clean energy.

This is hard work, requiring not just more expansive, finer-grained data than what we already gather on these relationships but the institutional capacity within the state to process it, sector by sector. Consultancies, firms, and think tanks all employ and develop personnel who can do pieces of this work today. The problem with this private sector data, as investor and energy specialist Alex Turnbull points out, is the lack of transparency and standardization needed to fully operationalize it. Instead, the state can and should take on some of these capacities in microeconomic data, like it did with macroeconomic data a century ago.

If we can get this right, it might be possible to ensure that a growing economy is one that can absorb a greater labor share of GDP without bottlenecks and price spikes. GDP was not invented overnight, and neither will our micro-accounting framework. But one day, we can hope that such information is as ubiquitous as its big brother.

■

Yakov Feygin is the associate director of the Future of Capitalism program at the Berggruen Institute and an associate editor at Noema Magazine.